Tom's Guide Verdict

This fee-free credit card offers seamless iPhone integration and an emphasis on security, but could use more cash-back categories and travel rewards.

Pros

- +

No fees

- +

Frustration-free Wallet app

- +

Seamless iPhone integration

Cons

- -

Cash-back limitations

- -

No travel perks

Why you can trust Tom's Guide Our writers and editors spend hours analyzing and reviewing products, services, and apps to help find what's best for you. Find out more about how we test, analyze, and rate.

Since I signed up for my Apple Card in mid-August, I’ve spent $2,288.98 using Apple’s new credit card, putting everything from my Apple Music subscription to my weekly grocery trips on the gleaming (OK, now slightly dingy) titanium white card. The cash back I’ve earned from those thousands is now just shy of $40.

And that’s my biggest problem with Apple Card, which is otherwise a perfectly fine credit card that costs nothing to use (other than interest charges, which I avoid by paying the card in full every month). The Apple Card’s perks just aren’t as good as with other credit cards, which offer travel rewards or higher cash-back percentages.

After two months with Apple Card, I’ve come to terms with the fact that it’s just not for me. But Apple’s credit card will appeal to some people, particularly those who value security and convenience over rewards.

Who is Apple Card for?

I travel often, both for work and for fun, and my preferred credit cards give me an easy way to rack up points that I can use to book flights or hotels. I have an American Express Platinum that gets me into airport lounges where I can work (and snack for free) and a Chase Sapphire Preferred that I use wherever AmEx isn’t accepted. Both cards require annual fees ($550 and $95, respectively), but the perks outweigh the costs.

For those who don’t want to pay an annual fee and/or don’t travel often, a fee-free, cash-back card like Apple Card makes sense. But it might not be the best option, depending on what you use your credit card for. Other cards, such as Chase Freedom, offer up to 5% cash-back in specific categories. Apple’s top tier cash-back is just 3%, and only in Apple stores and through select partners like Uber, Walgreens and T-Mobile. Otherwise, you’ll earn 2% back for using Apple Card via Apple Pay, and just 1% on purchases made with the physical Apple Card. It’s worth doing your research to find out which cash-back card is the right one for you.

Apple Card application and set-up

Applying for an Apple Card is easy: Simply open the Wallet app on your iPhone, tap the giant plus (+) sign in the top right corner, and start the process of entering your personally identifying details to see if Apple’s credit card partner, Goldman Sachs, deems you worthy of a credit line. Check out our step-by-step process to applying for an Apple Card.

In my case, approval was almost instantaneous, which was a pleasant surprise. Within 5 minutes of starting the application, my digital Apple Card was set up and ready to use in the Wallet app. I also set the card as my default for Apple Pay, which made it easy to place orders online and to use Apple Pay in stores. My physical card arrived days later, but I had already used it multiple times: ordering food from a delivery service, paying for groceries at my Apple Pay-compatible supermarket, and so on.

Using the Wallet app, I could also see down to the hour when my physical card was scheduled to be delivered. With other credit cards, it’s always a surprise.

The only problem I have with the Apple Card’s application process is that I can’t add my husband as an authorized user, as I usually do when I get a new credit card (and he does the same for me). I prefer to centralize our spending, which makes it easy to track and pay off each month, and I can imagine Apple implementing this in a way that would be convenient. They just haven’t done it yet.

Using the Apple Card

After two months of using Apple Card, I can say that this is the first credit card that has ever inspired me to use Apple Pay on a regular basis.

I know, I know, it’s weird. Using Apple Card via Apple Pay is the exact same as using Apple Pay with any other credit card. But I wanted the 2% cash back instead of just the 1% I would get using the physical card. Now I use Apple Pay everywhere I possibly can, which still isn’t everywhere, but I find myself surprised at how widespread Apple Pay acceptance is now.

The only time I had trouble using Apple Card was on a trip to Italy, where I found many places I visited either didn’t accept MasterCard or otherwise rejected the card. After hearing, “Your card was declined,” three times in one day, I switched to my Visa for the remainder of my vacation and resumed Apple Card use when I returned to the States. (I’m still not entirely sure why I had so many problems, though it may be due to the physical Apple Card’s unusual design.)

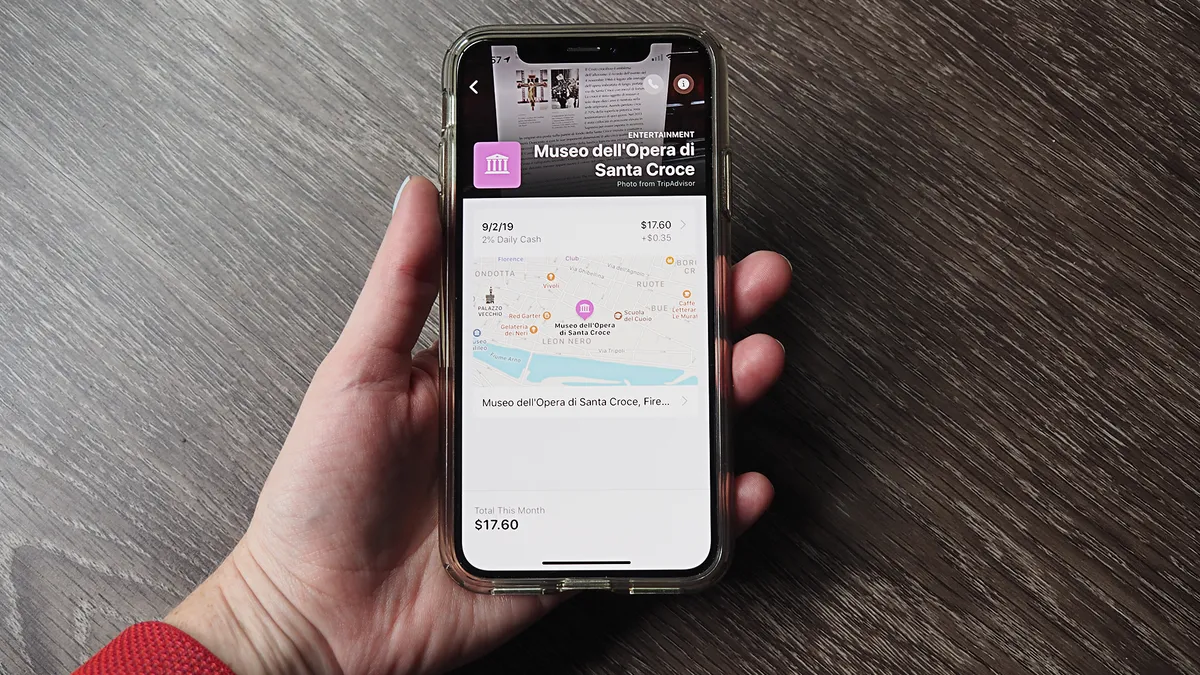

The Apple Card’s tight integration with the iPhone Wallet app makes it incredibly easy to track my spending and my cash-back earnings. For instance, when a transaction posts, the Wallet app sends a push notification telling me how much I earned. When it comes time to pay off the card each month, the app also tells me how much interest I’ll pay if I decide against paying the entire statement balance. (I have not paid interest, but it’s useful to know exactly how much it would cost me if I did.)

Apple Card benefits

One of my favorite things about Apple Card is that I still have no idea what my card number is — and neither does anyone else. That means it’ll be damn near impossible for someone to steal the number and use it to commit fraud. Every other credit card I’ve ever used has been compromised at one point or another, and now it just seems inevitable that I’ll have to report fraudulent transactions and change all my auto-pay information at least once a year. I shouldn’t have to worry about that with Apple Card.

When I use my Apple Card on the web, I simply use Apple Pay. Apple creates a number when you apply for your Apple Card and then stores it on your device’s Secure Element, which means no one can access it without your iPhone. I authenticate every transaction with Face ID. These layers of security make Apple Card more tempting to use than it otherwise would be.

Bottom line: Is Apple Card worth it?

Apple Card costs nothing to use, especially if you pay your balance off each month to avoid being charged interest. You’ll find better perks with other credit cards, but few offer the convenience and security of Apple Card. For those reasons, I recommend it.

That said, it’s not the credit card for me. The limited cash-back partners, the low percentage tiers and the lack of authorized users add up — Apple Card just doesn’t fit into my life. But for iPhone owners who don’t care about any of those things and just want a secure card that allows them to easily track their spending, Apple Card is a low-risk, near-perfect option. The extra couple bucks in cash-back every month is simply a bonus.